Managerial Accounting

Short notes

Definition of Management Accounting:

The Managerial Accounting is another name of Management Accounting s

Management accounting, therefore,is an integral part of organization process. It provides information essential for:

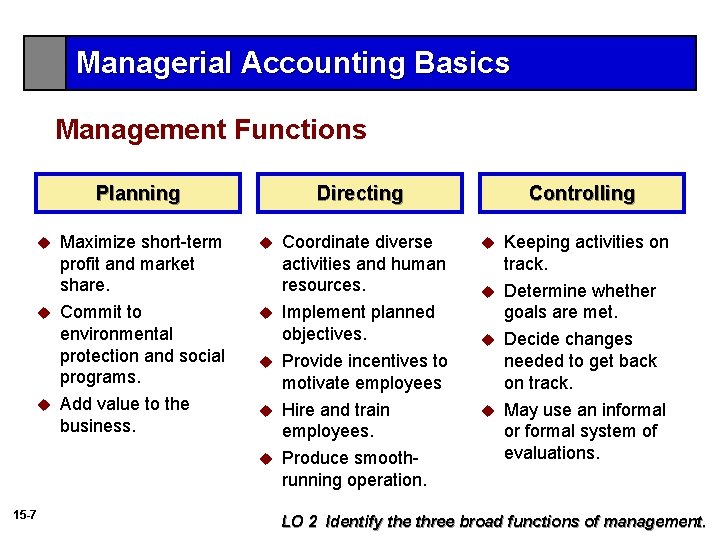

Controlling the current activities of an organisation

Planning its future strategies, tactics and operations

Optimizing the use of its resources

Measuring and evaluating performance

Reducing subjectivity in the decision making process and

Improving internal and external communication

Controllability: Management accounting facilitates the proper monitoring, analysis, comparison and interpretation of information which can be used constructively in the control, evaluation and corrective functions of management.

Reliability: Management accounting information must be of such quality that confidence can be placed in it. Its reliability to the user is dependent on its source, integrity and comprehensiveness. Interdependence:

Management accounting, in recognition of the increasing complexity of business, must access both external and internal information sources from interactive functions such as marketing, production, personnel, procurement, finance, etc.

Management accounting must ensure that flexibility is maintained in assembling and interpreting information. This facilitates the exploration and presentation, in a clear, understandable and timely manner, of as many alternatives as are necessary for impartial and confident decisions to be taken. The process is essentially forward looking and dynamic.

Stage 1 – Prior to 1950, the focus was on cost determination and financial control, through the use of budgeting and cost accounting technologies.

• Stage 2 – By 1965 the focus have been shifted to the provision of information for management planning and control, through the use of such technologies as decision analysis and responsibility accounting:

• Stage 3 – By 1985, attention was focused on the reduction of waste in resources used in business processes, through the use process analysis and cost management technologies.

• Stage 4 – By 1995, attention had shifted to the generation or creation of value, through the use of technologies which examine the drivers of customer value, shareholder value, and organizational innovation. While these four stages are recognizable, the process of change from one to another has been evolutionary.

• Cost determination and financial control

• Information for management Planning and control

• Reduction of waste of resources in business processes

• Creation of value through effective resource use

Comments

Post a Comment